India’s smartphone market has quietly grown up. What was once driven by first-time buyers hunting for the cheapest possible device is now shaped by upgrades, replacement cycles, and clearer consumer preferences. With more than 750 million internet users and over 95 percent of internet access coming from mobile devices, the smartphone has become India’s primary digital gateway rather than a discretionary purchase.

Shipment growth in 2024 remained moderate, according to industry trackers like Counterpoint and IDC, but that stability reflects maturity rather than weakness. Indian users are holding on to phones longer, often two to three years, and upgrading with intent. Camera performance, battery life, 5G compatibility, and long-term software support now weigh more heavily than just price. Festival sales and exchange offers still trigger buying surges; but the broader pattern shows a market that is settling into predictable, replacement-led demand rather than impulsive buying.

How Manufacturing Changed India’s Role in the Global Supply Chain

Perhaps the biggest structural shift in India’s smartphone market has happened behind the scenes. Over the last decade, domestic manufacturing has expanded rapidly under government-led incentives such as the Production Linked Incentive scheme. According to government electronics data, India’s mobile phone production value has grown from under ₹20,000 crore a decade ago to well over ₹4 lakh crore by FY24. Today, the vast majority of smartphones sold in India are assembled locally; and exports of India-made phones have surged year after year.

Global brands like Apple and Samsung now manufacture a significant share of their global smartphone output in India, not just for domestic consumption but for markets in Europe and North America. This shift has reduced import dependence, improved pricing efficiency, and created large-scale employment across assembly, logistics, and component ecosystems. More importantly, it has repositioned India from being merely one of the world’s largest smartphone buyers to becoming one of its most important production hubs.

Why 5G and Premium Phones Are Driving the Next Phase

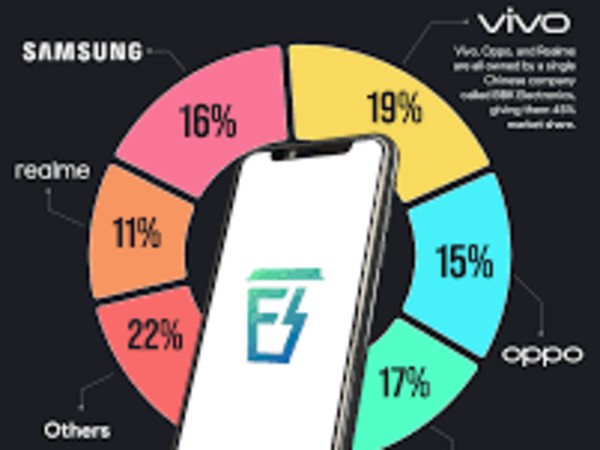

On the consumer side, the most visible change is premiumisation. While budget smartphones still dominate unit volumes, the fastest growth is happening in luxury bands. The nationwide rollout of 5G networks in 2024 accelerated this transition. Telecom data shows that 5G coverage expanded rapidly across urban and semi-urban regions, pushing consumers to view older 4G devices as outdated.

As a result, average selling prices have risen, even in a price-sensitive market like India. Industry reports indicate that the premium segment has reached record shipment levels, with Apple achieving its strongest-ever quarterly performance in India in 2024. This signals a clear shift in mindset: consumers are increasingly willing to pay more for long-term value, ecosystem reliability, and resale potential.

Competition, however, remains intense. Chinese and global brands continue to fight aggressively across mid-range and premium tiers through feature innovation and retail incentives. Looking ahead, analysts expect India’s smartphone market to grow less in sheer volume and more in value, driven by premium upgrades, export-led manufacturing, and India’s deeper integration into global technology supply chains.